TAKE CONTROL OF

YOUR TRADER TAXES

Use our intelligent app or turnkey service solutions to manage wash sale effects and prepare IRS-ready trader tax reporting.

Few things are worse than paying taxes on money you never made.

You’re a trader, you make intelligent trading decisions for success. Why should your trader tax results be determined by a broker-provided 1099-B that may be incomplete or even increase your tax liability?

TradeLog empowers traders with tools needed to do more than create tax reports:

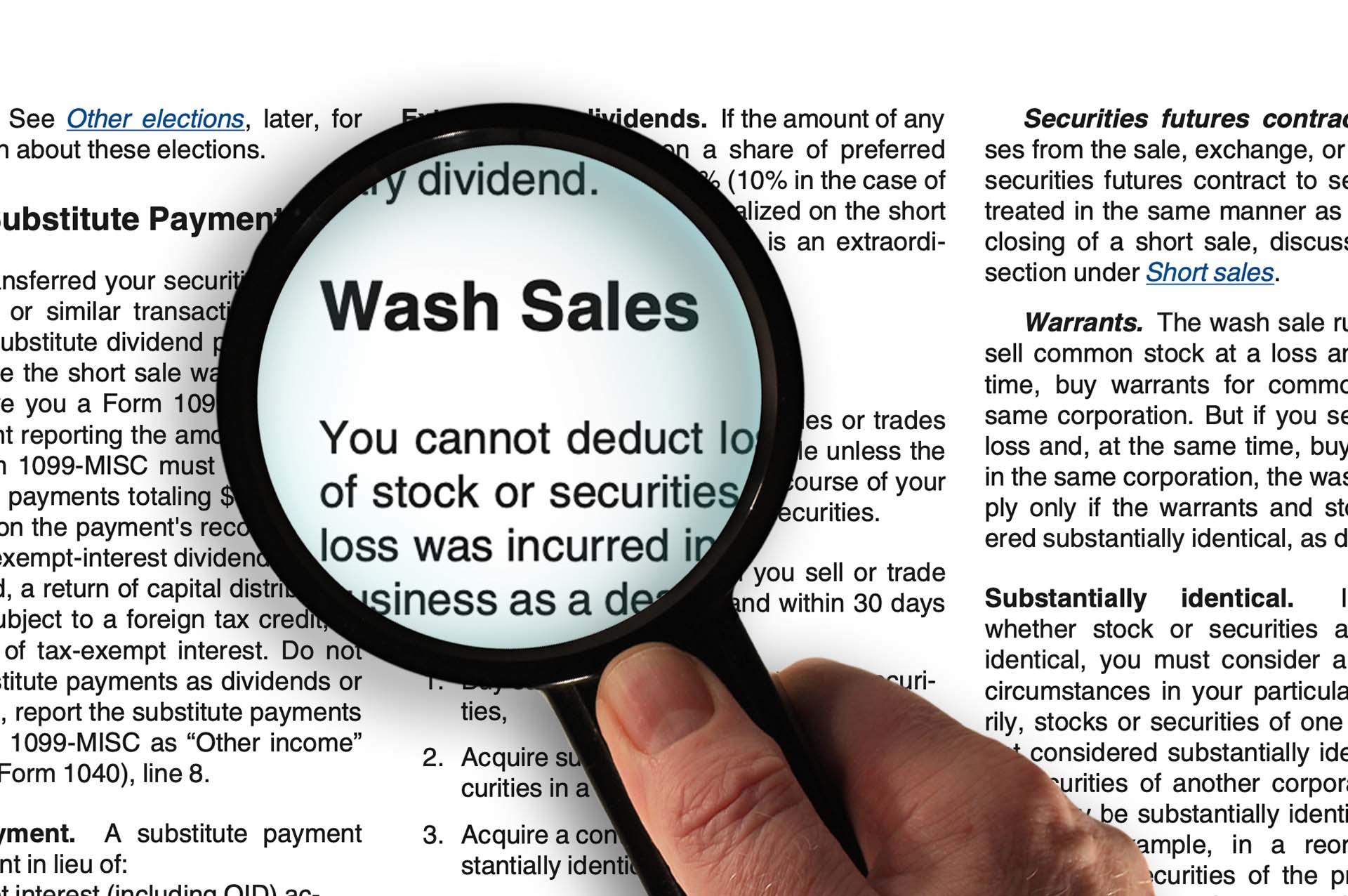

Take control of your wash sales

Take advantage of special tax rules

Switch to trader tax status

Wish someone else would just do it for you? We provide turnkey service solutions allowing you to focus your time on trading while we take care of the tax part.

It’s about more than just creating tax reports.

Trader taxes are complicated and we are committed to your success.

- Comprehensive Education Topics and Support Center

- Real technical support people who are TradeLog experts

- Trusted by thousands of traders and trader tax pros for over 23 years

- TradeLog’s reporting has never been rejected by the IRS

Get Started with TradeLog

Sign up for the

TradeLog Free Trial

Our 30-Day Free Trial allows you to preview TradeLog’s reporting with your accounts.

Download and start using

TradeLog for your accounts.

TradeLog runs on your PC, keeping your data secure wherever you store your files.

Purchase the one-year

subscription level you need

Opens full functionality and includes one File Key to unlock final end-of-year reporting.

Many traders think they can rely solely on broker-provided 1099-B for tax reporting, but you’re smarter than that!

Likely you are here because you learned the IRS requires traders make additional wash sale adjustments for common situations. Or, you found the 1099-B may increase tax liability – sometimes even causing traders to owe taxes when they actually lost money. Because the 1099-B lacks important details it can be impossible to make additional adjustments or even understand the results. And by the time it’s issued there is nothing you can do to control any harmful wash sale situations.